The first paycheck from a new job can feel oddly disappointing. You multiply your hourly wage by the number of hours you worked, expect one number, and then see a smaller deposit land in your account. Nothing mysterious has happened. The number you calculated is usually gross pay, while the amount you receive is net pay, sometimes called take-home pay.

That gap is one of the most practical economics lessons a worker can learn. A paycheck is not just a reward for hours worked. It is also a record of taxes, public programs, workplace benefits, and choices made on forms like the W-4. Once you know how to read it, a pay stub becomes less frustrating and more useful: it shows where your earnings went before the money reached your bank account.

Gross Pay Is the Starting Point, Not the Final Number

Gross pay is the amount earned before anything is taken out. For an hourly worker, it usually begins with a simple calculation: hourly rate times hours worked. If someone earns $16 an hour and works 20 hours, the gross pay for that week is $320. For a salaried worker, gross pay is usually the portion of an annual salary assigned to that pay period.

The complication is that gross pay can include more than ordinary hours. Overtime, bonuses, commissions, shift differentials, tips, and paid time off can all change the starting number. A worker who earns overtime may see a larger gross amount than expected, while someone who started halfway through a pay period may see a smaller one. The pay period itself also matters. Weekly, biweekly, semimonthly, and monthly pay schedules divide earnings differently, even when the annual income is the same.

Net pay is what remains after deductions. Some deductions are required by law, such as certain payroll taxes. Others may come from voluntary choices, such as health insurance, retirement contributions, or savings plans. That is why two people with the same wage can take home different amounts. Their gross pay may match, but their tax situation, benefits, and deductions may not.

Federal Income Tax Withholding Is an Estimate

One of the biggest deductions on many paychecks is federal income tax withholding. This is money an employer sends to the IRS during the year on the worker’s behalf. It is not the final tax bill by itself. It is an estimate based on the worker’s pay, filing status, and information entered on Form W-4.

That detail matters because withholding is not meant to be perfectly exact on every paycheck. The tax system works across the full year, while paychecks arrive in pieces. An employer uses IRS withholding methods to decide how much to hold back from each pay period. If too much is withheld during the year, the worker may receive a refund after filing a tax return. If too little is withheld, the worker may owe money later.

Form W-4 helps the employer make that estimate. New employees usually fill it out when they start a job, and workers can update it when their situation changes. Filing status, multiple jobs, dependents, credits, and extra withholding can all affect the amount taken out. A teenager with a summer job, a college student with two part-time jobs, and a full-time worker supporting a family may all need different withholding patterns.

This is why the word withholding can be confusing. The employer is not keeping the money as profit. The money is being sent ahead to cover expected income tax. The worker’s tax return later compares what was withheld with what was actually owed for the year.

Social Security and Medicare Taxes Come Out Separately

Federal income tax is not the only tax on a paycheck. Most workers also see deductions for Social Security and Medicare, often grouped under FICA. These payroll taxes support federal social insurance programs, and they are calculated differently from income tax withholding.

For wages paid in 2026, the employee Social Security tax rate is 6.2 percent on wages up to the annual wage base. The Social Security Administration lists the 2026 wage base as $184,500, meaning earnings above that limit are not subject to the Social Security portion for that year. Medicare tax works differently: the basic employee rate is 1.45 percent, and there is no general wage base limit for Medicare wages. Higher earners can also face an additional Medicare tax above certain thresholds.

For a first paycheck, the main thing to notice is that these payroll taxes are separate from federal income tax. A worker who has little or no federal income tax withheld may still see Social Security and Medicare taken out. That can surprise students and new workers who expected a small job to escape taxes entirely.

Employers also pay their own share of Social Security and Medicare taxes. That employer share usually does not appear as a deduction from the employee’s gross pay, but it is part of the broader cost of employing someone. From the worker’s point of view, the pay stub mainly shows the employee share being withheld from earnings.

Benefits and Voluntary Deductions Can Change Take-Home Pay

Not every deduction is a tax. Many pay stubs include items connected to workplace benefits or personal choices. Health insurance premiums, dental or vision coverage, retirement plan contributions, commuter benefits, union dues, charitable giving, and flexible spending accounts can all reduce the amount deposited into a bank account.

Some of these deductions happen before certain taxes are calculated, while others happen after taxes. That difference can change both taxable income and take-home pay. For example, some retirement or health-related deductions may reduce taxable wages for certain purposes, while a normal after-tax deduction simply comes out after taxes have already been figured. The details depend on the benefit and the rules attached to it.

Voluntary deductions can be good, but they should still be understood. A retirement contribution may lower the paycheck today while building savings for the future. A health insurance premium may reduce take-home pay while protecting against larger medical costs. A worker who only looks at the final deposit may miss the value of benefits being purchased through the paycheck.

There can also be required non-tax deductions in special situations, such as court-ordered garnishments. Other workplace deductions, such as uniforms or equipment, are regulated by wage laws and state rules. The U.S. Department of Labor notes that wage deductions can become a legal issue when they affect minimum wage or overtime protections. When a deduction looks unfamiliar, it is worth asking payroll or human resources what it means.

A Pay Stub Is a Map of the Money

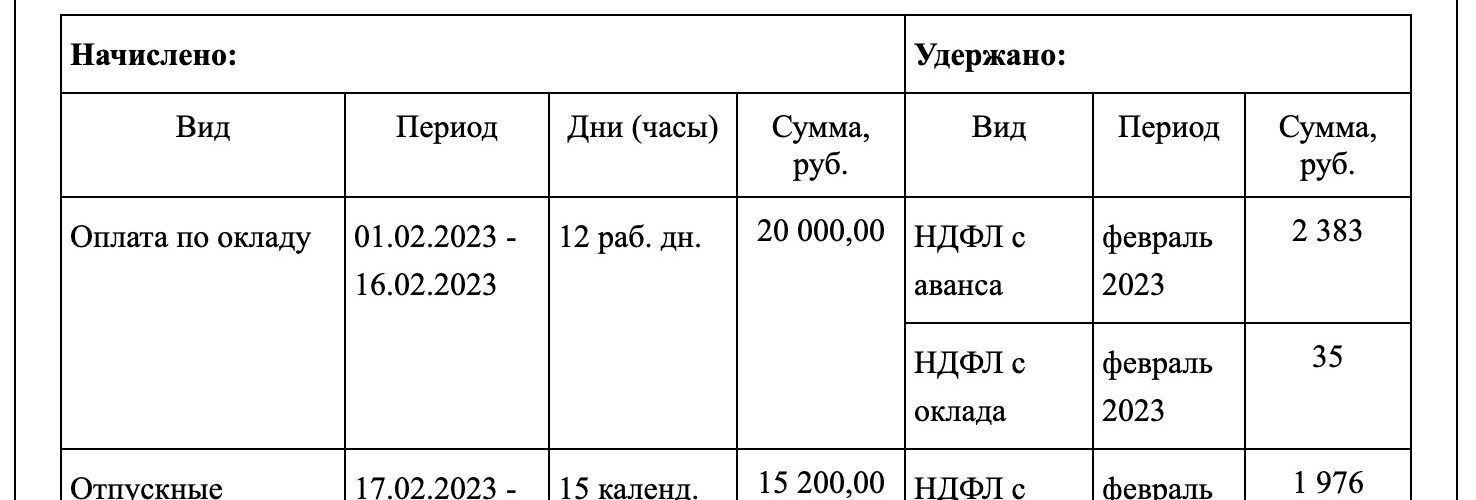

A pay stub usually separates the paycheck into sections. The exact layout varies by employer, but the same ideas appear again and again. The top often shows the worker’s name, pay period, pay date, and sometimes the number of hours worked. The earnings section lists gross pay, including regular hours, overtime, bonuses, or other forms of compensation.

The deductions section shows what was taken out. Taxes may appear as federal income tax, state income tax, local tax, Social Security, Medicare, or similar labels. Benefit deductions may appear under insurance, retirement, or other workplace plan names. Many pay stubs also show year-to-date totals, which add up earnings and deductions since the beginning of the calendar year.

Year-to-date numbers are especially useful because a single paycheck can be unusual. A bonus, missed shift, overtime week, or benefits change can make one pay period look different from the rest. The year-to-date column gives a broader view of how much has been earned, how much has been withheld, and how much has gone toward benefits over time.

Reading a pay stub also helps catch mistakes. Hours may be missing, overtime may be recorded incorrectly, or a deduction may appear after a worker thought it had been stopped. Small errors can add up if no one notices them. The habit of checking each pay stub is less about suspicion and more about knowing your own money.

Why the Smaller Number Still Teaches Something Useful

The gap between gross pay and net pay can feel like money disappearing, but it is better understood as money being routed. Some of it goes to tax systems that fund public programs. Some may go toward benefits that the worker chose or accepted. Some may be withheld now so the final tax filing later is less surprising.

For students and new workers, the most helpful habit is to budget from net pay, not gross pay. An hourly wage is useful for comparing jobs, but take-home pay is what pays for transportation, food, savings, and personal expenses. A job that looks generous on paper may feel different once commuting costs, taxes, and deductions are included.

Over time, paycheck math becomes easier to predict. A worker learns what a normal deposit looks like, how overtime changes it, and which deductions are fixed or flexible. That knowledge makes it easier to compare job offers, set savings goals, spot payroll errors, and understand why a tax refund or tax bill happens later.

A paycheck is smaller than the wage calculation suggests because wages pass through a system before they arrive. The important thing is not to memorize every tax rule. It is to understand the route: gross pay starts the journey, required taxes and chosen deductions shape it, and net pay is the amount that finally reaches the worker. Once that route is visible, the paycheck stops being a mystery and starts becoming a tool.

Add comment